SX/EW US$/lb 0.31 Leaching US$/lb 0.41 G&A US$/lb 0.08 Total LOM Operating Cost US$/lb 1.22 C1 Cash Costs US$/lb payable 1.23 AISC (All-in Sustaining Costs) US$/lb payable 1.87 Copper price US$/lb 2.82 Economic Indicators Post-tax operating cash flow US$ millions 237.7 Post-tax NPV (8% disc) US$ millions 71.4 Post-tax NPV (5% disc) US$ millions 92.6 Post-tax IRR % 28 Cumulative Cash Flow US$ millions 139.8

Casa Grande, AZ, March 10, 2020 - Elim Mining Incorporated (“Elim” or the “Company”), a private copper exploration and development company, is pleased to announce results of a Preliminary Economic Assessment (“PEA”) on its Cactus Mine Stockpile in the revitalized Santa Cruz porphyry copper district in Arizona, USA. The PEA demonstrates a robust 8-year conventional run of mine copper heap leach, solvent extraction and electrowinning process facility to produce copper cathodes at LME Grade A quality standards with attractive economics using conservative base-case assumptions.

John Antwi, Elim President and CEO commented, “I am proud of the work the team has done to progress the stockpile project to the scoping study level within a year since Elim’s incorporation. The completed study provides a measure of Phase 1 in an 8-year operation, with both low operating costs and capital requirements. As a past-producing mine, within a known porphyry copper district, the Elim team has a huge advantage which includes immediate access to infrastructure and workforce in addition to the exceptional mineral development potential.”

He continued, “The Cactus Stockpile processing project allows Elim the opportunity to self-fund a portion of the larger Phase 2 and 3 exploration and development of the multi-billion pound historic copper potential. These activities include additional exploration drilling, in-situ Mineral Resource Reporting, and Preliminary Economic Assessments for the Cactus Mine East Deposit, Cactus Mine West pit layback and the Parks/Salyer Projects, expected by Q4 2020. Management will take advantage of the operational synergies that the various deposits and mineralization styles present to further lower operating costs and capital expenditures.”

PEA HIGHLIGHTS

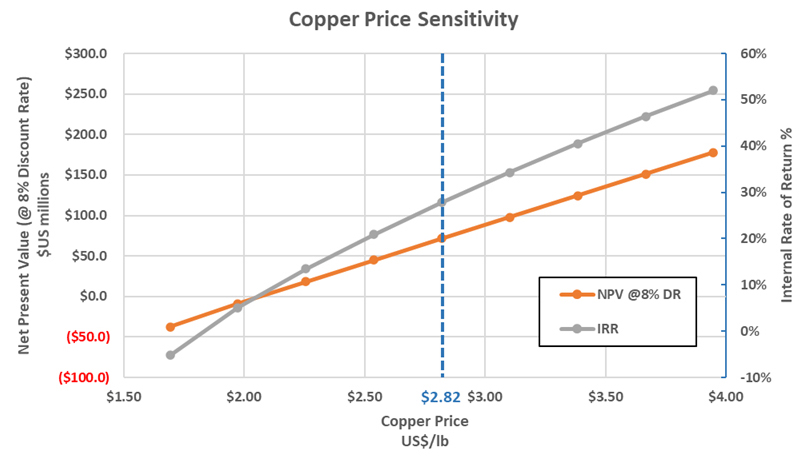

Base case parameters assume a copper price of US$2.82/lb.

Low upfront costs

- Initial capital costs of $71.4 M, including $19.2 M for pad construction, ponds and pipeline, $52.1 M to purchase and install the SX/EW plant and including $9.3 M for contingencies

Simple Operation

- Heap leach operation processing 75,500,000 short tons (“st”) @ 0.168% total copper (“TCu”) over 8 years

- Total copper production of 182.4 million lbs of copper as cathode • Average annual heap leach processing rate of 30,000 st from the onsite SX/EW plant

- Average acid and cyanide soluble combined recoveries of 83.3% and total copper recovery of 71.9%

- Onsite heap leaching and SX/EW plant

Strong standalone project economics

- Base Case after-tax NPV (8%) of $71.4 M with an IRR of 28% and a 3.3 year payback

- Cumulative Free Cash Flow of $140 million

- Average annual steady state cash flow of $31 million

- Average life of mine cash costs(1) of $1.23/lb of copper produced ($2.94 per ton processed) and AISC of $1.87/lb of copper produced

Optimization opportunities ahead

- General understanding of ASARCO’s pit mining schedule, coincident with mineral placement with the stockpile

- Potential to reduce trucking fees via conveyor belt

- Synergies with future potential pit layback, regarding SX/EW plant, workforce and equipment

(1) Cash cost includes mining cost, mine-level G&A, mill and refining cost

Project Location

The Project is located is located 40 road miles (71 km) south southeast of the Greater Phoenix metropolitan area and approximately 3 miles (4.8 km) northwest of the city of Casa Grande, Pinal County, Arizona, USA. The historic Sacaton Mine is 10 miles (16 km) due west of the Interstate 10 (I-10) freeway. Total site area is approximately 2,465 acres (6,090 hectares).

Geology and Mineralization

The Stockpile (5,000 ft x 4,900 ft x 100 ft) was established by ASARCO’s Sacaton open pit mine which extracted 38 Mt, producing 398 Mlbs Copper, 1.4 Moz Silver, 30 koz Gold with an 84% recovery. The operation ran from 1972-1984. All oxide copper mineralization, and sulfide copper mineralization below the working grade control cutoff of 0.3% Cu, were deposited to the waste dump. The resulting stockpile contains three vertical lifts of each ~40 ft height. Therefore, the separate lifts vertically represent different periods of time in the mining sequence.

The Cactus Mine Project is located within the prolific Santa Cruz porphyry copper district and comprises Elim’s Cactus East and West historic deposits and the Parks/Salyer showing. The district has been dismembered and displaced by Tertiary extensional faulting. The deposit has a complex history of oxidation and leaching which resulted in the formation of a chalcocite blanket.

The chalcocite blanket in the orebody is irregular in thickness, grade, and continuity. These irregularities are caused by tilting, post-enrichment oxidation, and possibly by fault offsets.

The later stage of oxidation and leaching modified the blanket by oxidizing portions of it in place and mobilizing some of the chalcocite to a greater depth. Substantial quantities of oxidized copper minerals are found in the oxidized zone.

Mineral Resources Included in the Stockpile Project Mine Plan

The total resources included in the PEA mine plan (the “Mine Plan”) are shown in the table below. The mineral resource used in the PEA includes approximately 5,120 ft (1,561 m) of drilling undertaken in 2019. There is indication, with the initial 700 ft spaced drilling program, that some zones of unmineralized lithologies such as conglomerate may be identifiable and separable as waste zones. The drill hole intercepts were composited to 10 ft composite lengths for CuAS, CuCN, and TCu assaying methodology. The mineralized stockpile material was assigned a material type of “stockpile” in three lifts corresponding to the order of placement on the stockpile. There are two small volume alluvium dumps located within the mineralized stockpile volume. Their blocks were set to a material type of “alluvium”. The stockpile immediately to the north of the mineralized stockpile was also incorporated into the block model extents and assigned a material type of “alluvium”. Mineral resources meeting the cut-off grade of 0.09% TSOL Cu (total soluble copper) are reported as Inferred resource below. The Company plans to infill drill later this year as it works towards a Pre-Feasibility.

Mineral Resources Included in the Mine Plan5

| CLASS | CUTOFF TSOL Cu | Tons (Mt) | Grade (%) | Pounds Cu (Million lbs) | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| CuAS | CuCN | TSOL_Cu | TCU | CuAS | CuCN | TSOL_Cu | TCu | |||

| Inferred | 0.09 | 75.5 | 0.121 | 0.024 | 0.145 | 0.168 | 182.6 | 36.2 | 218.8 | 253.5 |

Notes:

- There is a reasonable probability of eventual economic extraction of this resource using sulfuric acid leaching and SXEW recover at a TSOl_Cu cutoff of 0.09% and a copper price of $2.82/lb. (based on the NASDAQ 3 year trailing average);

- Mineral resources, which are not mineral reserves, do not have demonstrated economic viability. The estimate of mineral resources may be materially affected by environmental, permitting, legal, title, sociopolitical, marketing, or other relevant factors; and,

- The quantity and grade of reported inferred mineral resources in this estimation are uncertain in nature and there is insufficient exploration to define these inferred mineral resources as an indicated or measured mineral resource; it is uncertain if further exploration will result in upgrading them to an indicated or measured classification.

Mining, Processing and Production Plan

The PEA contemplates an 8-year heap leach operation to process oxide material from the Cactus Stockpile using mining contractors, followed by crushing, agglomeration and heap leaching. The resulting pregnant leach solution (“PLS”) from the heap leach ponds will be pumped for processing in a modular design copper SX/EW plant capable of producing up to 14,000 tpy of copper cathodes with a design PLS flow of up to 3,000 gpm and PLS feed grade at approximately 3.0 gpl copper. Water and raffinate would be managed onsite. Overall material contained in the mine plan developed by Samuel Engineering has 75.5 mt of heap leach material, with an average grade of 0.168% TCu.

Metallurgy

The potential stockpile resources to be processed are 75.5 Mt at a grade of 0.168% TCu. An initial mining rate of 30,000 tpd of leach pad feed is anticipated.

Copper recovery is based on preliminary scoping metallurgical testing and similar project benchmarks. Recovery of 71.9% of TCu is projected to be achieved over a 2 year leaching cycle based on an 85% recovery of the acid soluble copper (CuAS) copper content and 75% recovery of cyanide soluble (CuCN) copper content as determined using a sequential assaying methodology also used for the resource grade determinations. The study considers using 13.6 pounds per ton of net acid consumption, based on bottle roll testing results, and at a processing cost component of $0.81/ short ton.

| Copper Recovery Assumptions and Distributions | |||||

|---|---|---|---|---|---|

| Leach Recovery | Distribution | YR 1 | YR 2 | ||

| CuAS (sequential) | 85% | Average Recovery | 75% | 10% | |

| CuCN (sequential) | 75% | Average Recovery | 35% | 40% | |

| Effective Recovery | 83.3% | of Soluble Copper Content | |||

| 71.9% | of Total Copper | ||||

Column leach testing in closed circuit with solvent extraction is planned for these materials and will provide a more considered value for acid consumption in future and correlation to the bottle roll results.

Stockpile Infrastructure

The Cactus Mine site is currently accessible via an existing network of roads, designed for accommodating heavy equipment and other vehicles. Power for the Project will be drawn from the existing network of transmission lines and substation located onsite.

The site infrastructure for the Project will include fencing, network of onsite roads, water and raffinate management ponds, a solvent extraction plant including ponds, tanks and pumps, electrowinning treatment facility and tanks, 120kV line with tie into nearby HV infrastructure, various site buildings including warehouse and operations offices. The contractor for mining will provide any additional required facilities.

The Stockpile project is estimated to provide direct employment 41 hourly and staff personnel across the different phases of the life of mine, which would be expected to be drawn from the surrounding communities to provide support to the project. During the construction phase, the peak work force is expected to be approximately 41 plus the mining contractor. The construction and operation will provide additional employment opportunities to the surrounding communities. Later Phases of the broader Cactus Mine will significantly increase the requirements of hourly and staff personnel.

Stockpile Project Economic and Sensitivity Analysis

The operating assumptions for the financial model for the Stockpile are as follows:

| Production | Units | LOM Total |

|---|---|---|

| Life of mine | years | 8 |

| Annual tons processed (LOM average) | Ktons | 10,950 |

| Total tons processed | Ktons | 75,500 |

| Net revenue from sales | US$ millions | 510.7 |

| LOM Operating Costs (per ton) | ||

| Mining | US$/t rock | 1.01 |

| SX/EW | US$/t rock | 0.75 |

| Leaching | US$/t rock | 0.99 |

| G&A | US$/t rock | 0.19 |

| Total LOM Operating Cost | US$/t rock | 2.94 |

| LOM Operating Costs (per pound) | ||

| Mining | US$/lb | 0.42 |

| SX/EW | US$/lb | 0.31 |

| Leaching | US$/lb | 0.41 |

| G&A | US$/lb | 0.08 |

| Total LOM Operating Cost | US$/lb | 1.22 |

| C1 Cash Costs | US$/lb payable | 1.23 |

| AISC (All-in Sustaining Costs) | US$/lb payable | 1.87 |

| Copper price | US$/lb | 2.82 |

| Economic Indicators | ||

| Post-tax operating cash flow | US$ millions | 237.7 |

| Post-tax NPV (8% disc) | US$ millions | 71.4 |

| Post-tax NPV (5% disc) | US$ millions | 92.6 |

| Post-tax IRR | % | 28 |

| Cumulative Cash Flow | US$ millions | 139.8 |

(1) Cash cost includes mining cost, mine-level G&A, mill and refining cost

The initial and sustaining capital costs are presented as follows:

| Capital costs | US$ millions |

|---|---|

| Initial capital costs (pre-production) | 71.4 |

| Sustaining capital costs | 20.4 |

| Total LOM Capital Costs | 91.4 |

Breakdown of the capital cost is shown below:

| Item | Subtotal Direct US$M |

Subtotal Indirect US$M |

Contingency 15% |

Total Cost US$M |

|---|---|---|---|---|

| Mine & Equipment | 0 | 0 | 0 | 0 |

| Leach Pad, Ponds and Pipelines | 14.6 | 2.1 | 2.5 | 19.2 |

| SX/EW Facility | 31.9 | 13.5 | 6.8 | 52.1 |

| Total | 46.5 | 15.6 | 9.3 | 71.3 |

The construction cost of Phase 2 of the Leach Pad, approximately $20.4 MM, is carried as a sustaining cost in Year 3 of the Economic Model. No other sustaining capital is anticipated for the facilities given the project operating life of 7 to 8 years and contractor mining.

A sensitivity analysis was performed, to test the impact of changes to copper price included in the economic model, with the following results:

Over the coming months, the Company will be focused on:

- Permitting:

- Permitting an operation on private land requires the following critical path permits:

- Pinal Air Quality Control Permit (Permit Approved)

- Arizona Department of Environmental Quality (ADEQ) Aquifer Protection Permit (APP) (Pre-Application Meeting has been held with ADEQ and awaiting final design input)

- Arizona Pollutant Discharge Elimination System (AZPDES) permits (construction and Multi‐Sector General Permit) (Permit Submitted)

- ADEQ State of Arizona Clean Water Act Section 401 Water Quality Certification (Permit Submitted)

- Arizona State Mine Inspector Reclamation Plan (to be applied for)

- Permitting an operation on private land requires the following critical path permits:

- Stockpile Project:

- Completing a detailed Project Development schedule which will provide a critical path to a production decision, including detailed engineering and permitting

- Resource definition sonic drilling in the Stockpile

- Cactus West, Cactus East and Parks/Salyer:

- Resource modelling of satellite deposits with a goal of releasing an updated mineral resource estimate and PEA

- Ongoing environmental baseline work to support the update of existing permits and filing for additional permits that may be required.

The Company’s PEA is based upon a database of 55 sonic drill holes with an effective date of March 1, 2020. All drill holes informed the resource estimate with an overall average spacing of 700 ft (213 m).

Mineral Resources are not Mineral Reserves and do not have demonstrated economic viability. There is no certainty that all or any part of the Mineral Resources estimated will be converted into Mineral Reserves. The estimate of Mineral Resources may be materially affected by changes in environmental, permitting, legal, title, taxation, socio-political, marketing, or other relevant issues that may arise subsequent to the effective date. The CIM definitions were followed for the classification of Indicated and Inferred Mineral Resources. The quantity and grade of reported Inferred Mineral Resources in this estimation are uncertain in nature and there has been insufficient exploration to define these Inferred Mineral Resources as an Indicated Mineral Resource and it is uncertain if further exploration will result in upgrading them to an Indicated Mineral Resource category. All figures have been rounded to reflect the relative precision of the estimates.

Qualified Persons and NI43-101 Disclosure

The PEA was prepared by Samuel Engineering Inc. in conjunction with Stantec Consulting Services Inc., supported by the Elim Mining project team. This PEA is preliminary in nature and includes inferred mineral resources that are too speculative geologically to have economic considerations applied to them that would enable them to be categorized as mineral reserves. There is no certainty that PEA results will be realized. Mineral resources are not mineral reserves and do not have demonstrated economic viability.

Technical aspects of this news release have been reviewed and verified by Allan Schappert – CPG, who is a qualified person as defined by National Instrument 43-101– Standards of Disclosure for Mineral Projects. Mine design, planning, estimation and engineering aspects of this news release have been reviewed and verified by James Sorensen, FAusIMM, Samuel Engineering, who is a qualified person as defined by National Instrument 43-101. A Technical Report pursuant to National Instrument 43-101 guidelines for the Preliminary Economic Assessment will be posted to the Company’s website within 45 days.

About Elim Mining Incorporated (www.elimmining.com | www.cactusmine.com)

Elim Mining Incorporated is a private mineral resource development company with headquarters in Reno, Nevada and Phoenix, Arizona. Elim is rooted in the identification, acquisition, exploration, development and sustainable production of precious and base metal properties in well-known geographic regions. The company seeks assets with significant potential for proven and probable mineral reserves. Elim is managed by mining executives with over 210 years of experience in mine operations and business. With a history and reputation for strategically launching, revitalizing, and leading multi-million-dollar mining organizations, the team has achieved tremendous growth and value for investors in a socially and environmentally responsible manner.

For more information:

ohn Antwi, President and CEO

520-858-0600

jantwi@elimmining.com

Alison Dwoskin, Investor Relations

647-233-4348

adwoskin@elimmining.com

Forward-Looking Statements

Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Elim to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Factors that could affect the outcome include, among others: future prices and the supply of metals; the results of drilling; inability to raise the money necessary to incur the expenditures required to retain and advance the properties; environmental liabilities (known and unknown); general business, economic, competitive, political and social uncertainties; results of exploration programs; accidents, labour disputes and other risks of the mining industry; political instability, terrorism, insurrection or war; or delays in obtaining governmental approvals, projected cash operating costs, failure to obtain regulatory or shareholder approvals.

Although Elim has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results to differ from those anticipated, estimated or intended. Forward-looking statements contained herein are made as of the date of this news release and Elim disclaims any obligation to update any forward-looking statements, whether as a result of new information, future events or results or otherwise, except as required by applicable securities laws